.png)

It’s easy to see a credit card as “free money” and spending more than your means. But if you're not careful, you could wind up paying a lot in fees and interest, hurt your credit score, and really hurt your wallet.

But you’re in luck - Skyla has been helping people in our local communities with lending and credit usage for over 60 years. This is our bread and butter!

To make sure you’re well educated about a new credit card, we’ll walk through how credit cards work, how to properly use a credit card, what to look out for, and more. To top it off, I'll also share signs that can help you determine if you're ready to be a credit cardholder.

if you want to jump to any section, here’s what we’ll be covering:

|

|

how do credit cards work?

how do credit cards work?

A credit card is basically a loan in card form. A lender issues you a line of credit up to a certain amount (your limit), and you can spend however much of it you’d like. The appealing part of a credit card (compared to a personal loan) is that you only repay what you use. But – don’t forget – when repaying the lender, you may incur additional fees and interest. Plus, there isn’t a set term, so you can keep your credit line open indefinitely

Psst… when making a payment on a credit card, the lender usually allows you a grace period between 21-30 days after the close of the billing cycle to repay the money used without interest. After the grace period, you’ll start accruing interest charges unless you have a credit card that offers a 0% interest rate. |

In the United States, credit cards operate under four different networks (also called card associations) – Visa, Mastercard, American Express, and Discover. The networks are what link the funds being transferred from credit card holder to merchant.

credit card types: unsecured vs secured

credit card types: unsecured vs secured

When looking for a credit card, there are two types to choose from. An unsecured credit card is the most common type of credit card and does not require any collateral in order to open/get approved. Basically, the lender only has your word that you’ll repay what you charge to the credit card and / or the fees and interest that accrue. Opposite of that is a secured credit card. A secured credit card is backed by collateral – typically money deposited and held by the lender – which often serves as your credit limit and reduces the risk for the lender.

When looking for a credit card, there are two types to choose from. An unsecured credit card is the most common type of credit card and does not require any collateral in order to open/get approved. Basically, the lender only has your word that you’ll repay what you charge to the credit card and / or the fees and interest that accrue. Opposite of that is a secured credit card. A secured credit card is backed by collateral – typically money deposited and held by the lender – which often serves as your credit limit and reduces the risk for the lender.

QUICK TIP: If you have credit issues, no credit history, and/or a desire not to overspend, a secured credit card could be your perfect fit! It helps to build or rebuild your credit, and your approval odds are much higher than with unsecured credit cards. The security deposit you make when opening the account protects you in case you miss a credit card payment. But don't miss your payment! The credit card issuer reports account information to the major credit bureaus each month. That positive monthly payment report can help you improve your credit score. |

tips before getting a credit card

tips before getting a credit card

- Check your credit score and report: When applying for a credit card, your credit score and report play significant roles when lenders determine whether to approve your application or not. Lenders pay attention to your payment history, the amount of money you owe on other accounts, the types of credit you have (if any), and more. Order your free credit report at annualcreditreport.com. If you notice any incorrect information, contact the credit bureau and the organization that provided the wrong information as soon as possible.

QUICK TIP: Want to learn more about what goes into your credit score and how it’s analyzed by lenders? Check out why your credit score is so important. |

- Have a steady income to pay off credit card debt: It's always best to have your own income source to pay off your credit card and not rely on anyone else to help you pay it.

- Shop around for credit cards: It's essential that you shop around / do your research before choosing the credit card that’s right for you. This means comparing interest rates and fees (think annual fees, foreign transaction fees, late payment fees, etc.) and loyalty rewards you might be able to take advantage of, like cash back or redeemable rewards points for travel or merchandise. Always know what you're getting into!

QUICK TIP |

- Know how to read a Schumer Box: When shopping for a credit card or reading your credit card agreement, you're going to come across a table or a box that includes a summary of your credit card terms, rates, fees, and more. This contains all the information you'll need when managing your credit card. Here's a closer look at what the Schumer Box will include:

- Your Annual Percentage Rate (APR), which indicates the amount of interest you'll be charged on your purchase(s) if you don’t pay your credit card off in full each month.

- The flat fee or annual fee

- Minimum payments

- How your outstanding balance will be calculated

- Number of days in a billing cycle

how can i use a credit card responsibly?

how can i use a credit card responsibly?

- Only charge what you can afford: A credit card is meant to help build your credit, so it makes sense to use your credit card, but only with purchases that you can actually afford or those larger items that you have a solid plan on how you’ll pay them off. That way, you’re less likely to get yourself in credit card debt trouble.

- Keep your credit card utilization low: Stay way below your credit limit! Credit utilization is the amount you currently owe divided by your credit limit, which is expressed as a percentage. If you have more than one credit card, any auto loans, student loans, or other types of debt, lenders will combine these totals to calculate your credit utilization and determine your creditworthiness. The Consumer Financial Protection Bureau recommends you stay below 30% of your credit limit. Other experts suggest having a 10% threshold.

QUICK TIP: So, if your limit for one card is $1,000, then keep your balance under $300. If you have more than one credit card where one has a $3,300 limit with a $3,300 balance and a second card has a limit of $6,700 with no balance, you're right at the 30% mark ($3,000 of an available $10,000) which is right where you want to be. |

For every 1% of available credit you use on your credit card, you lose roughly 1 point off of your credit score. In theory, if you have a 600 credit score with no credit cards and you open a $5,000 limit credit card, your score could increase up to 700. If you then used $2,500 of that balance, then your credit score would drop to 650

- Pay off your balance (or pay more than the minimum payment): Yes, lenders allow you to just make a minimum payment, but that will only add more interest to your balance. If possible, pay your balance off in full each month. If you can't do that, then at least pay more than the minimum payment so you're reducing both your principal and interest.

- Pay your bill on time: Being on time with your payment is critical. If you're late, not only will you be charged a late fee, but your late payment will be reported to the credit bureaus and will hurt your credit score.

- Never skip a payment: If you accidentally missed a payment, you're on the path to damaging your credit. Once you realize it, make your payment as soon as possible.

- Pay attention to your monthly credit card statement: When you have a credit card, you're sent a statement showing a

summary of how you've used your card for the specific billing period. It includes an overview of account activity, payment information (like your new balance for the month), payment due date, credit limit, available credit, and much more. If you’re aiming to be a responsible credit card user, pay close attention to your statement, so you're always in the loop. Check for any problems. Fraud happens way more often than you think. If you don't recognize a charge, report it right away. Reporting fraudulent charges prevents you from paying for things you did not buy.

summary of how you've used your card for the specific billing period. It includes an overview of account activity, payment information (like your new balance for the month), payment due date, credit limit, available credit, and much more. If you’re aiming to be a responsible credit card user, pay close attention to your statement, so you're always in the loop. Check for any problems. Fraud happens way more often than you think. If you don't recognize a charge, report it right away. Reporting fraudulent charges prevents you from paying for things you did not buy. - Set up automatic payments: Having automatic payments set up to pay off your balance is a sure way of avoiding missed payments. This is certainly not mandatory, but it will definitely help if you're afraid you'll miss a payment. Psst... Contact your lender to see if a direct deposit can be set up so a portion of your paycheck each month can go toward your credit card balance. Again, you don't have to do this, but it can help pay down debt from big purchase items.

- Stick to a budget: To ensure you're not overspending or getting close to your credit limit, a budget will help you stay on track. Set a spending limit. If you budgeted your expenses to $500 pay off any credit card debt you have.

- Know your credit card fees: Depending on the credit card you get, it may come with fees. Knowing those fees will help you stay prepared when paying off your credit card balance. Typical credit card fees include an annual fee, interest charges, late payment fee (if you're late on a payment), Balance transaction fee, etc. Psst...You can check the credit card terms, such as interest rates and fees, before applying for the credit card. And don’t forget about that handy Schumer box!

QUICK TIP: Want a full list of credit card do's and don'ts so you're better prepared on how to best use a credit card when you get one? Here's a full breakdown perfect for you. |

what types of interest do credit cards charge?

what types of interest do credit cards charge?

Earlier I mentioned interest when getting a credit card. Interest is what lenders charge you for borrowing money. Well – to make things a bit more complicated – there are 2 types of interest: compound interest and simple interest. For credit cards, lenders typically use compound interest calculated daily. How does that affect you? Think of it as accruing interest on top of interest. Let me explain….

definitions

compounding period

annual percentage rate (apr):

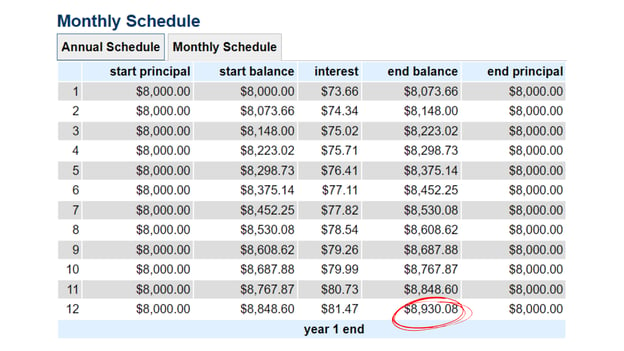

So… let's say you did a bit of shopping last month and charged your brand-new credit card $8,000, which has an 11% APR (Annual Percentage Rate) on purchases, interest compounds daily, and your billing cycle is 30 days. That means you could be paying $73.66 per month in interest (or roughly $930.08 a year). But, because your interest amount changes daily, you could actually pay more than $73.66 per month. Here's a breakdown of what that could look like.

QUICK TIP: In this example, an interest rate of 11.00% compounded daily is equivalent to an annual rate of 11.626%. |

Did you notice the interest amount increase as you go month to month? Well, that increase can be due to a variety of factors, especially if you carry over a balance from month to month (also known as a revolving balance). This not only affects your existing balance but also affects any new purchases that may be posted to the credit card account.

If you're wondering how long it will take you to pay off your credit card or trying to decide if it's a good idea to use your credit card for a big purchase? Use this super helpful credit card payoff calculator to get your answer!

QUICK TIP: Did you know there are credit cards that offer offer a 0% APR deals? Yep! Here’s what happens if you have a 0% APR credit card.. |

what important credit card terms should i know?

what important credit card terms should i know?

annual fee

annual percentage rate (apr)

available credit

average daily balance

balance transfers

cash advances

credit card limit

grace period

security code (cvv)

here's how to tell if you need a credit card so you can move forward

Although you don't need a credit card to function financially, having one certainly does help when it's used properly. You’re able to build your credit using a credit card, earn rewards such as cashback and points on purchases, provide additional buying power where you can make purchases without having physical cash, and more. But credit cards have their drawbacks, too. Like paying interest and fees if you carry a balance from month to month, you could miss a payment, or spend more than anticipated on your card, affecting your credit score and long-term financial success.

Although you don't need a credit card to function financially, having one certainly does help when it's used properly. You’re able to build your credit using a credit card, earn rewards such as cashback and points on purchases, provide additional buying power where you can make purchases without having physical cash, and more. But credit cards have their drawbacks, too. Like paying interest and fees if you carry a balance from month to month, you could miss a payment, or spend more than anticipated on your card, affecting your credit score and long-term financial success.

Before opening a credit card, make sure you have a steady income and enough money rolling in to cover any fees and interest charges that may come with your future card. If possible, check your credit report before applying for the card. Since you're entitled to a free credit report every year, you can read through it and make sure everything is on the up and up. And if anything doesn't look right, you can get ahead of it by reporting it to the credit bureau (here's more on how to fix errors on your credit reports).

If you're struggling to determine if you're ready for a credit card, here's a quick chart to help you decide:

%20(700%20%C3%97%20450%20px).png?width=700&name=7Youre%20ready%20(950%20%C3%97%20768%20px)%20(700%20%C3%97%20450%20px).png)

Need help budgeting? I have just the thing(s) to get you started! Grab this Smart Budgeting Kit to help get your finances right on track or check out the basics to building your budget to start your budgeting journey.

Get the Credit Card Facts

Get the Credit Card Facts

This is what to expect when getting a credit card so you can properly prepare and enjoy your credit card today.

Know when to apply for a credit card

Know when to apply for a credit card

Apply for a credit card when you're ready - here's what that means.

Check How Credit Card Applications Impact Your Score

Check How Credit Card Applications Impact Your Score

Your credit score is affected when applying for a credit card but here's how you can stay on top of it.